We make boring business stories sparkle.

How Loan Interest Is Calculated: A Simple Guide for Business Owners

A simple guide for Singapore business owners to understand how loan interest, fees, cash received and total repayment affect the real cost of borrowing.

A loan can look simple because the lender gives you one monthly repayment.

But the real cost is not just the monthly instalment. The real cost is the difference between the cash you receive and everything you must pay back, including interest and fees.

This guide explains loan interest in simple English for Singapore business owners. Use it together with the SBO Loan Calculator when you compare offers.

The simple way to think about loan cost

When you borrow money, there are four numbers to look at:

- Cash received: how much money actually reaches your bank account.

- Monthly repayment: how much you pay every month.

- Total amount repaid: all instalments and fees added together.

- Total cost: total amount repaid minus cash received.

If you remember only one thing, remember this:

A cheaper-looking monthly repayment is not always a cheaper loan.

A longer loan can lower the monthly repayment but increase the total interest. A loan with deducted fees can give you less cash than you think. A flat-rate loan can look cheaper than it really is if you compare only the advertised rate.

What does loan interest actually mean?

Interest is the price you pay for using someone else’s money.

If you borrow S$50,000, the lender wants the S$50,000 back plus extra money for lending it to you. That extra money is interest.

But lenders do not always calculate interest in the same way. This is where many business owners get confused.

Principal

The principal is the loan amount used for the repayment calculation.

If the loan is S$50,000, the principal is usually S$50,000. But if some fees are added into the loan, the principal used for repayment may be higher.

Interest rate

The interest rate tells you how fast interest is charged.

A lender may quote 8% per year, 1% per month, or a flat rate. You need to know how that rate is applied before comparing offers.

Tenure

Tenure means how long you take to repay the loan.

A 12-month loan and a 60-month loan with the same principal and rate will not have the same total cost. The longer you borrow, the longer interest has time to build.

Fees

Fees are easy to miss because they may not appear inside the interest rate.

Common examples include:

- processing fee,

- admin fee,

- annual fee,

- monthly servicing fee,

- legal or documentation fee,

- late payment fee.

For licensed moneylenders, MinLaw’s borrower guide sets rules on permitted interest, late interest, fees and total borrowing costs. Always verify the lender on the Registry of Moneylenders list before borrowing.

Flat rate vs reducing balance: why the same rate can mean different cost

This is one of the biggest traps in loan comparison.

Two loans can both say “8% per year”, but the cost can be different depending on whether the rate is flat or reducing balance.

Reducing balance interest

Reducing balance interest is charged on the outstanding loan balance.

As you repay the loan, the outstanding balance becomes smaller. Interest is then charged on a smaller amount.

This is common for many bank-style term loans.

Flat rate interest

Flat rate interest is charged on the original loan amount for the whole loan period.

Even though your outstanding balance goes down every month, the interest calculation still starts from the original principal.

This is why a flat rate often looks lower than the real cost. A flat rate is not the same as an effective annual cost.

Loan term | Simple meaning | Why it matters |

|---|---|---|

Reducing balance rate | Interest is based on the unpaid loan balance. | Usually better for comparing bank-style loans. |

Flat rate | Interest is based on the original loan amount. | Can look cheap but produce a higher real cost. |

Processing fee | A fee charged when the loan is approved or disbursed. | If deducted upfront, you receive less cash. |

Monthly fee | A recurring admin or servicing fee. | Raises your monthly cash outflow even if the instalment looks fine. |

Effective cost | A better estimate of the real annual cost after timing and fees. | Helps compare loans more fairly. |

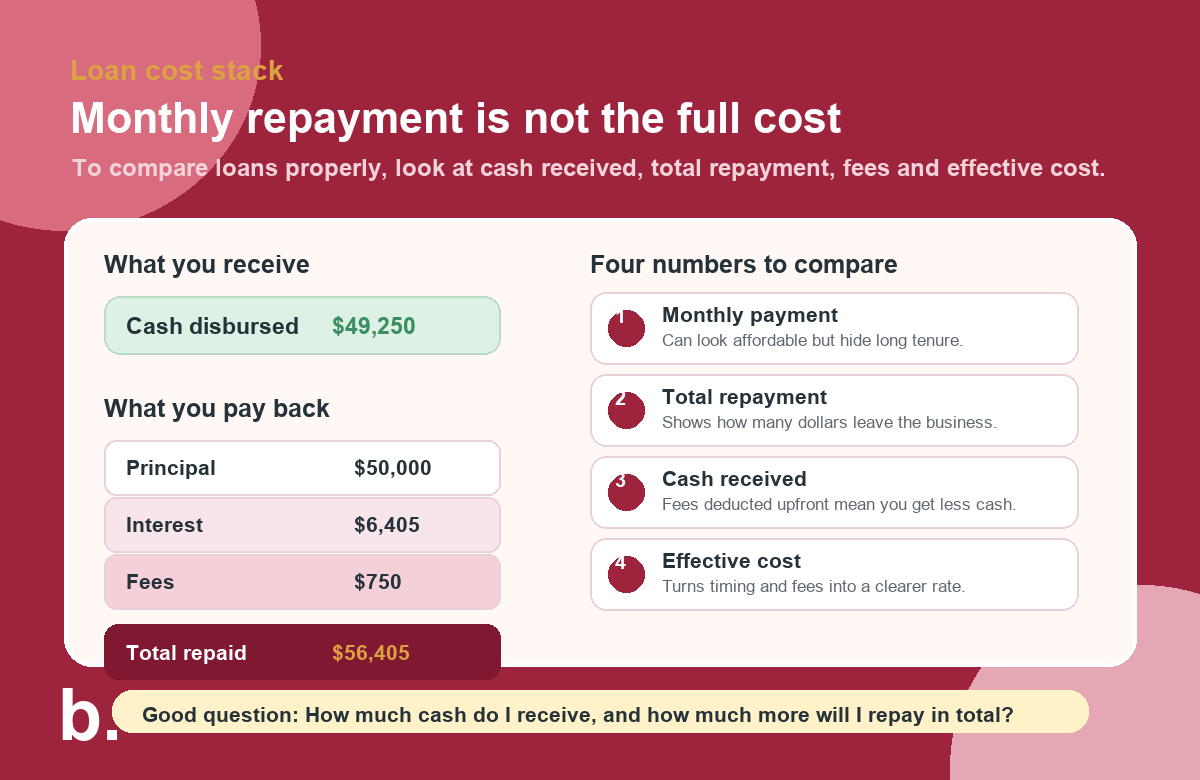

A simple example: the monthly payment is not the whole story

Imagine a business owner takes a loan with these terms:

- Loan amount: S$50,000

- Tenure: 36 months

- Quoted reducing balance rate: 8% per year

- Processing fee: 1.5%

- Fee treatment: deducted from disbursement

The monthly repayment may look manageable. But look at the full cost stack.

Item | Estimated amount | What it means |

|---|---|---|

Loan amount | S$50,000 | The principal used for repayment. |

Processing fee | S$750 | 1.5% of S$50,000. |

Cash received | S$49,250 | The fee is deducted upfront, so less cash reaches the business. |

Monthly repayment | About S$1,566.82 | The amount paid each month before any extra monthly fee. |

Total amount repaid | About S$56,405.46 | All monthly repayments over 36 months. |

Total cost above cash received | About S$7,155.46 | The real dollar cost compared with what the business actually received. |

That is why a loan should not be judged only by whether the monthly repayment fits this month.

The better question is:

“How much cash do I receive today, and how much more must I repay in total?”

You can test this example in the SBO Loan Calculator by entering S$50,000, 36 months, 8%, a 1.5% processing fee and “deducted from disbursement”.

Three ways fees change the real cost of a loan

Fees matter because they change either your cash received or your repayment amount.

1. Fees deducted from disbursement

This means the lender approves one amount but gives you less cash.

Example: you borrow S$50,000, but a S$750 fee is deducted. You receive S$49,250, but you may still repay based on S$50,000.

This raises your real cost because you are paying for money you did not actually receive.

2. Fees paid separately upfront

This means you pay the fee from your own cash before or when the loan starts.

Your loan balance may stay the same, but your cash position is still worse on day one.

3. Fees added to the loan principal

This means the fee becomes part of the loan amount.

It may feel painless because you do not pay it immediately, but you may pay interest on the fee too.

Why lower monthly repayment can still be expensive

Many business owners ask, “Can I afford the monthly instalment?” That is important, but it is only the first check.

A lower monthly repayment can happen because:

- the interest rate is lower,

- the loan period is longer,

- fees are hidden outside the instalment, or

- the loan structure pushes cost into the future.

Only the first reason is clearly good. The others may make the loan feel comfortable while increasing the total cost.

What business owners should check before signing

Before taking any business loan, personal loan or licensed moneylender loan, write these numbers down.

Loan cost checklist

- How much cash will enter my bank account?

- What is the monthly repayment?

- Are there monthly fees on top of the instalment?

- What is the total amount repaid over the full tenure?

- What is the total interest?

- What are all upfront and recurring fees?

- Is the quoted rate flat or reducing balance?

- What happens if I repay early?

- What happens if I pay late?

- Does anyone give a personal guarantee?

For general financial planning, MoneySense reminds consumers to plan their finances and avoid over-borrowing. Business owners should be even more careful because business cash flow can be uneven.

When a loan is worth considering

A loan is not automatically bad. Debt can be useful when it solves a clear timing problem or funds work that can repay the debt.

Good reasons may include:

- a confirmed project where payment comes after delivery,

- stock or materials needed for signed orders,

- temporary cash-flow gaps caused by slow customer payments,

- equipment that improves capacity or margin,

- refinancing expensive debt into a cheaper, clearer structure.

Bad reasons include:

- borrowing to cover losses with no recovery plan,

- borrowing because approval is fast, not because the loan is suitable,

- using debt to delay hard decisions about pricing, staffing or costs,

- borrowing without checking total repayment,

- taking a personal loan because the business cannot qualify for any business financing.

If you are deciding between business financing and personal borrowing, read our guide to business loan options in Singapore and our guide on personal loans for business owners.

How to use a loan calculator properly

A calculator is useful only if you enter the right inputs.

When using the SBO Loan Calculator, do not stop after typing the loan amount and interest rate.

Fill in:

- the loan amount,

- the tenure in months,

- whether the rate is flat or reducing balance,

- the quoted annual rate,

- processing fee percentage,

- fixed upfront fee,

- whether fees are deducted, paid upfront or financed,

- monthly admin fee,

- monthly cash available for repayment,

- existing monthly debt payments.

Then compare the results, especially:

- cash received,

- monthly cash outflow,

- total amount repaid,

- total cost above cash received,

- effective annual cost,

- affordability ratio.

Bottom line

Loan interest is not just a percentage printed on a brochure.

The true cost depends on the loan amount, interest method, tenure, fees, fee treatment, cash received and repayment timing.

Before signing, make the loan compete on full cost, not only monthly instalment. If you cannot explain the total cost in one sentence, pause and calculate again.

Use the SBO Loan Calculator to estimate monthly repayment, fees, total repayment and effective cost before comparing offers.

Frequently Asked Questions

How is loan interest calculated in simple terms?

Loan interest is the cost of borrowing money. It can be calculated on the outstanding balance, as with reducing balance loans, or on the original loan amount, as with flat rate loans. The total cost also depends on tenure and fees.

Why is monthly repayment not enough to compare loans?

Monthly repayment does not show how much cash you actually receive, how many months you pay, what fees are charged, or the total amount repaid. A lower monthly repayment can still cost more if the tenure is longer or fees are high.

What is the difference between flat rate and reducing balance interest?

Reducing balance interest is charged on the unpaid loan balance, so interest falls as the balance falls. Flat rate interest is charged on the original loan amount for the full tenure, so the advertised rate can look lower than the real cost.

What loan number should a business owner check first?

Start with cash received and total amount repaid. Then check monthly cash outflow and effective annual cost. This shows both the immediate cash benefit and the full repayment burden.

Where can I estimate the full cost of a loan?

Use the SBO Loan Calculator to enter loan amount, tenure, rate type, fees and fee treatment. It estimates monthly repayment, cash received, total repayment, total cost and effective annual cost.

Explore More Content

Table of Content