We make boring business stories sparkle.

10 Business Loan Options in Singapore for SME Cash Flow

A practical listicle comparing business loan options, grants and personal loans for Singapore SME owners facing a cash-flow crunch.

When cash gets tight, many Singapore business owners ask the wrong first question: “Where can I get money fast?”

The better question is: “What type of funding matches the problem I am trying to solve?” A personal loan, business term loan, overdraft, invoice financing, trade loan, grant, and government-supported loan all behave differently. Some are useful for a short cash-flow crunch. Some are better for growth. Some should not be used when the business is already bleeding.

This listicle compares common business loan options in Singapore, how they differ from personal loans, where grants fit, and how owners should think before borrowing.

Quick answer: business loan or personal loan?

If the money is for the business, start with business financing first. A business loan keeps the purpose, documents, repayment plan, and accounting treatment closer to the company. A personal loan may be faster, but it puts the owner personally on the hook.

That does not mean business loans are always easy. Banks and finance providers will still check cash flow, bank statements, company age, directors, credit records, revenue, profitability, and the purpose of funds. But if the business has real revenue, proper records, and a clear use case, a business facility is usually the cleaner first option.

Question | Business loan is usually better | Personal loan may be considered |

|---|---|---|

What is the money for? | Inventory, payroll timing, equipment, trade, receivables, expansion | Very small short-term gap where business loan processing is impractical |

Who should repay? | The business, from business cash flow | The owner, from personal income or savings buffer |

What documents support it? | Bank statements, invoices, contracts, financial statements, tax records | Personal income proof, credit profile, Notice of Assessment, CPF or bank records |

Main risk | Business cash flow cannot support instalments | Owner carries personal debt even if the business fails |

Best use | Commercial need with measurable repayment source | Emergency bridge only after cheaper business options are checked |

1. SME Working Capital Loan under Enterprise Financing Scheme

The Enterprise Financing Scheme is Enterprise Singapore’s financing framework for local enterprises. It covers areas such as working capital loans, fixed asset loans, trade loans, project loans, green loans, venture debt, and merger and acquisition loans.

For a cash-flow crunch, the SME Working Capital Loan is the most relevant EFS category because it is meant for daily operational cash-flow needs. EnterpriseSG shares default risk with participating financial institutions, but the bank or financial institution still assesses and approves the loan.

Best for

- SMEs with real operating history and a temporary working capital gap.

- Businesses that need cash for payroll timing, supplier payments, rent, or operations while receivables are coming in.

- Companies with proper bank statements, financial records, and a credible repayment plan.

Approval likelihood

Moderate to stronger if the business has operating history, visible revenue, clean bank records, and a specific use of funds. Lower if the company has weak cash flow, repeated returned payments, poor documentation, or no realistic repayment source.

Pros

- Purpose-built for business cash flow.

- Government risk sharing may improve lender appetite for eligible enterprises.

- Keeps the financing discussion anchored to business operations instead of personal borrowing.

Cons

- Not automatic. A participating financial institution must still approve the application.

- May require directors’ guarantees, financial statements, bank records, and credit checks.

- Not a fix for a business that has no path back to positive cash flow.

2. Normal bank business term loan

A business term loan is a lump sum borrowed by the company and repaid over a fixed period. It can be used for working capital, expansion, renovation, equipment, marketing, or other approved business purposes depending on the lender.

Best for

- Established SMEs with stable revenue and decent bank balances.

- Planned cash needs where the owner can compare offers instead of rushing.

- Projects with a clear payback logic, such as a contract, equipment upgrade, or controlled expansion.

Approval likelihood

Stronger for companies with at least a few years of records, steady deposits, manageable existing debt, and clean director credit. Lower for young companies, volatile cash flow, recent losses, or weak personal credit of directors.

Pros

- Structured monthly repayment makes cash-flow planning clearer.

- Can provide a larger amount than many personal loans.

- May strengthen the company’s banking relationship if handled well.

Cons

- Processing can take time.

- Approval may be strict during a crunch, especially after bank balances have already weakened.

- Directors may still need to provide personal guarantees, so personal risk may not disappear.

3. Overdraft or revolving credit line

An overdraft or revolving business credit line gives access to funds up to an approved limit. Interest is typically charged on the amount used, not the whole approved limit.

Best for

- Uneven monthly cash flow where receivables and payables do not line up neatly.

- Seasonal businesses that need short bursts of liquidity.

- Companies disciplined enough to reduce the balance when cash comes in.

Approval likelihood

Moderate when the business already has a banking relationship and healthy account conduct. Lower when the company applies only after overdrawing accounts, missing payments, or showing distress.

Pros

- Flexible drawdown and repayment.

- Useful for short timing gaps.

- May cost less than repeatedly taking small emergency loans if managed well.

Cons

- Easy to treat as permanent debt.

- Limit can be reduced or reviewed by the lender.

- Requires discipline; otherwise it hides poor collections or weak margins.

4. Invoice financing

Invoice financing allows a business to receive cash against unpaid customer invoices. It is useful when the work is done, the invoice is valid, and the customer is likely to pay, but the payment term is slow.

Best for

- B2B businesses with invoices from credible customers.

- Companies waiting 30, 60, or 90 days for customer payment.

- Businesses that need to fund payroll, suppliers, or the next job while waiting for receivables.

Approval likelihood

Stronger when invoices are from reputable customers, amounts are clear, and there are no disputes. Lower when invoices are old, disputed, concentrated in one weak customer, or tied to incomplete work.

Pros

- Matches the loan to a specific receivable.

- Can be faster than a broad business term loan.

- Useful for growing companies that are profitable but cash-stretched by slow payment terms.

Cons

- Not useful without valid invoices.

- Fees can add up if used constantly.

- Some arrangements may involve customer notification, depending on structure.

For a deeper explanation, see our guide to invoice financing in Singapore.

5. Trade financing

Trade financing supports import, export, inventory, and supplier payment cycles. It can help businesses pay suppliers, secure goods, or bridge time between shipment and customer payment.

Best for

- Importers, exporters, distributors, wholesalers, and product businesses.

- Companies with purchase orders, supplier invoices, shipping documents, or confirmed customer demand.

- Businesses where the financing follows a real trade transaction.

Approval likelihood

Moderate to stronger when trade documents, supplier relationships, and customer orders are clear. Lower when the business is buying speculative stock without evidence of demand.

Pros

- Fits the cash cycle of product and trading businesses.

- Can help secure inventory without using all available cash.

- May be supported under the Enterprise Financing Scheme’s trade loan category for eligible businesses.

Cons

- Requires documents and transaction visibility.

- Inventory risk remains with the business if goods do not sell.

- Currency, shipping, supplier, and customer risks must be managed.

6. Equipment loan, fixed asset loan, or hire purchase

When the business needs vehicles, machinery, kitchen equipment, production tools, computers, or other assets, a fixed asset loan or hire purchase arrangement may fit better than a general cash loan.

Best for

- Assets that are necessary to operate or increase capacity.

- Equipment with a clear link to revenue, productivity, or cost savings.

- Businesses that want repayments to match the useful life of the asset.

Approval likelihood

Moderate when the asset is sensible, the business can afford repayments, and there is documentation such as quotations. Lower when the equipment is discretionary, over-sized, or unrelated to cash generation.

Pros

- Clear purpose and collateral logic.

- Can preserve working capital for operations.

- May be easier to justify than borrowing for general expenses.

Cons

- You still need enough cash flow to service the asset.

- Equipment can become underused if demand is overestimated.

- Early termination or repossession terms can be painful.

7. Business credit card or charge card

A business credit card is not a proper working capital plan, but it can help with short expense timing, employee controls, subscriptions, travel, and procurement.

Best for

- Short-term expenses that will be paid in full by the due date.

- Controlled staff spending and receipt tracking.

- Online software, ads, subscriptions, and travel expenses.

Approval likelihood

Moderate for owners or companies with acceptable income, credit profile, and account conduct. Lower if the business or director already has heavy unsecured debt.

Pros

- Fast and convenient for day-to-day spending.

- Useful expense controls and records.

- Rewards or rebates may help if the balance is paid in full.

Cons

- Expensive if balances are rolled.

- Not suitable for payroll, rent, or long cash-flow gaps.

- Can blur personal and business liability depending on the card structure.

Compare this against our guide to business credit cards in Singapore.

8. Grants such as PSG, EDG and MRA

A grant is not a loan. It usually reimburses or supports approved project costs, subject to eligibility, approval, claim rules, and documentation. Grants are useful when the project fits the scheme, but they are usually not fast cash for a crisis.

EnterpriseSG says existing grants such as PSG, EDG and MRA remain accessible until EDGE launches in the second half of 2026. Businesses should verify the latest scheme terms before applying.

Common grant examples

- Productivity Solutions Grant: supports pre-approved IT solutions and equipment, with up to 50% support for local SMEs and a stated cap of S$30,000.

- Enterprise Development Grant: supports projects to upgrade, innovate, grow and transform, including qualifying consultancy, software, equipment and internal manpower costs.

- Market Readiness Assistance Grant: supports overseas market promotion, business development and market set-up, with enhanced support of up to 70% from 1 April 2026 and a stated cap of S$100,000 per company per new market.

Approval likelihood

Stronger when the project clearly matches the scheme, the company meets eligibility, no payment or contract has been made before application where prohibited, and documents are complete. Lower when the project is already started, vague, not supportable, or mainly intended to rescue cash flow.

Pros

- Does not create loan repayment obligations when approved and claimed properly.

- Can reduce the cost of productivity, transformation, overseas expansion, or approved equipment projects.

- Encourages structured project planning.

Cons

- Not instant cash.

- Often requires approval before signing, paying, or starting work.

- Claim documents, audit, milestones, and reimbursement timing can affect cash flow.

- Not suitable for paying overdue rent, payroll arrears, old supplier debt, or general losses.

For broader grant planning, see our guides to Singapore business grants, PSG, and EDG.

9. Owner capital, shareholder loan, or director loan

Sometimes the cleanest funding is not a bank loan at all. The owner, shareholders, or directors may inject capital or lend money to the company. This can be useful when speed matters and the business is still viable.

Best for

- Short-term rescue funding where owners understand the downside.

- Businesses with partners who can document contributions clearly.

- Cases where bank financing is not suitable yet, but the company has a believable recovery plan.

Approval likelihood

Depends on owner resources, not lender approval. The real issue is whether the owner should put more money into the business and how that money is documented.

Pros

- Fast if owners have funds.

- Can be more flexible than external debt.

- May signal commitment to lenders or partners if the business later applies for financing.

Cons

- Personal wealth is at risk.

- Shareholder disputes can arise if contributions are not documented.

- It can delay a necessary decision to restructure or close a failing business.

10. Personal loan as a last-mile option

A personal loan may be quick, but it should not be the default funding source for business needs. The borrower is the individual, not the company. If the business does not recover, the owner still owes the money.

Best for

- Small, temporary gaps where business financing is not practical.

- Owners with stable personal income and a clear repayment fallback.

- Emergency bridging where the business case is specific and documented.

Approval likelihood

Depends mainly on the owner’s personal income, credit profile, and existing debt. This can make approval easier for some owners, but it also means the business problem becomes a personal debt problem.

Pros

- Can be faster than a full business loan application.

- May require fewer company documents.

- Useful for very small emergency gaps when repayment is certain.

Cons

- Personal liability remains even if the company fails.

- Can damage personal credit if repayments are missed.

- Often hides business problems instead of solving them.

- Can create accounting confusion if the money is transferred into the company without proper documentation.

Read the companion guide: Should Business Owners Take a Personal Loan in Singapore?

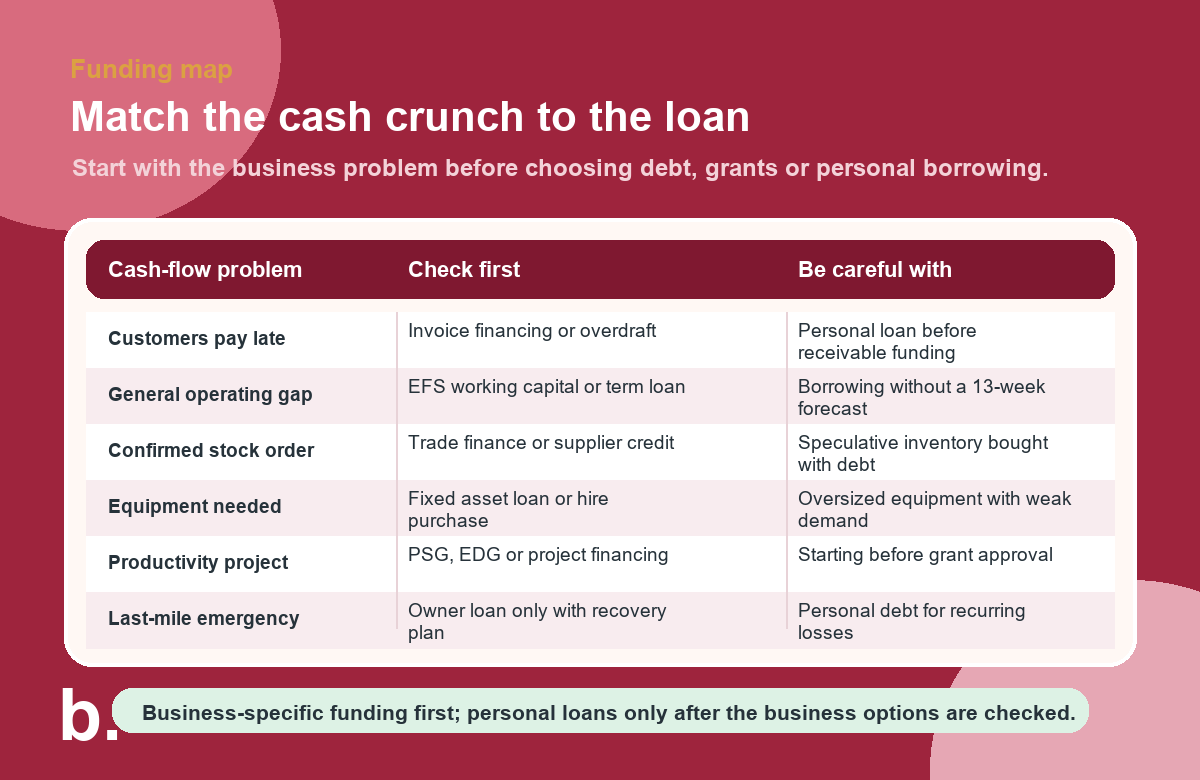

Which option fits which cash-flow problem?

The right funding choice depends on the root cause of the crunch. A slow-paying customer, a signed purchase order, an equipment breakdown, and a loss-making business should not be funded the same way.

Business situation | Options to check first | Usually avoid |

|---|---|---|

Waiting for good customers to pay invoices | Invoice financing, overdraft, working capital loan | Personal loan before checking receivable-based funding |

Need stock for confirmed orders | Trade financing, supplier credit, working capital loan | Buying speculative stock with expensive debt |

Equipment breakdown affects sales | Equipment loan, fixed asset loan, short working capital bridge | Long-term debt for equipment that does not improve revenue |

Digital tool or productivity upgrade | PSG, EDG, business loan if cash timing is needed | Starting before grant approval when retrospective claims are not allowed |

Overseas expansion project | MRA, EDG, trade loan, project loan | Personal loan for an untested overseas bet |

Recurring monthly losses | Cost cuts, repricing, restructuring, professional advice | More debt without fixing margins or sales |

Urgent owner-funded rescue | Shareholder loan, documented director loan, recovery plan | Undocumented personal transfers and emotional borrowing |

Good reasons to take a business loan

A good loan should improve the business after the loan, not merely postpone stress. Good reasons usually share three traits: the purpose is specific, the repayment source is visible, and the business changes for the better.

- Bridging a timing gap. You have receivables coming in, but payroll or suppliers are due first.

- Fulfilling signed work. You need materials, manpower, or logistics to deliver a confirmed order or contract.

- Buying productive equipment. The asset increases capacity, reduces cost, or protects revenue.

- Improving cash conversion. The loan helps shorten delivery, billing, collection, or inventory cycles.

- Replacing expensive debt with cheaper structured debt. This only makes sense if the total cost falls and the borrower stops adding new debt.

- Funding an approved project. The business has a grant-supported or lender-supported project with clear milestones and claims.

Bad reasons to borrow

Debt becomes dangerous when it funds avoidance instead of recovery. These are common red flags:

- Borrowing because sales “should recover soon” without signed orders, invoices, or a pipeline that can be verified.

- Covering repeated monthly losses without fixing pricing, headcount, rent, marketing efficiency, or gross margin.

- Taking a personal loan because the business was rejected without understanding why the business was rejected.

- Using grants as a reason to spend on a project the business does not truly need.

- Borrowing to avoid hard conversations with landlords, suppliers, lenders, shareholders, or staff.

- Borrowing without a 13-week cash-flow forecast. If you cannot see the next quarter, you are guessing.

Pre-loan checklist for business owners

Before applying, prepare the business case as if you were explaining it to a skeptical lender. That discipline helps even if you decide not to borrow.

- Define the crunch. Is it receivables timing, inventory, a one-off emergency, growth, or structural loss?

- Match the facility. Use invoice financing for invoices, trade finance for trade, equipment finance for assets, and grants for eligible projects.

- Prepare documents. Gather bank statements, ACRA profile, financial statements or management accounts, invoices, contracts, quotations, tax documents, and director details.

- Compare total cost. Include interest, processing fees, late charges, guarantee risk, early repayment terms, and time cost.

- Stress-test repayment. Check whether the business can pay if sales are 20% to 30% lower or customers pay late.

- Check grant timing. Do not sign, pay, or start work before approval if the grant rules prohibit retrospective applications.

- Document owner money. If directors or shareholders inject funds, record whether it is capital, a shareholder loan, a director loan, or reimbursement.

Frequently Asked Questions

What business loan should an SME check first during a cash-flow crunch?

Start with the cause of the crunch. If customers are slow to pay, check invoice financing. If the need is general working capital, check a business working capital loan or EFS-supported option. If it is a project, check whether a grant or asset loan fits better.

Are government-supported loans easier to get?

They can improve lender appetite for eligible enterprises because of risk sharing, but approval is not automatic. Participating financial institutions still assess the business, directors, repayment ability, and documents.

Are grants better than business loans?

Grants are better for eligible projects because they do not create normal loan repayments, but they are not instant cash and usually require approval, project completion, claims, and documentation. They are not a replacement for emergency working capital.

When should a business owner use a personal loan instead?

Only when the amount is small, the need is temporary, business financing is impractical, and the owner can repay personally even if the business recovery is delayed. It should not be used to hide recurring losses.

What improves the probability of business loan approval?

Clean bank statements, stable revenue, manageable debt, proper financial records, clear loan purpose, signed contracts or invoices, and a realistic repayment plan all improve the application quality.

The bottom line

Business owners should not treat all borrowing as the same. A cash crunch caused by slow receivables may need invoice financing. A confirmed trade order may need trade finance. A productivity upgrade may fit PSG or EDG. General operating pressure may fit a working capital loan, but only if the business can repay.

A personal loan is the emergency back pocket, not the main funding strategy. Use it only when the business case is small, short term, and repayable from personal resources if things go wrong.

The best funding decision is not the fastest approval. It is the option that matches the business problem, protects the owner from unnecessary personal risk, and leaves the business stronger after the money is used.

Explore More Content

Table of Content