We make boring business stories sparkle.

Cash Flow Management for Singapore SMEs: A Simple Owner Dashboard

A simple cash-flow dashboard for Singapore SME owners who want better visibility over cash, invoices, bills and runway.

Many small businesses fail in the gap between profit and cash. The sales look healthy, the team is busy, but supplier bills, salaries, CPF, tax, rent and software renewals still need cash on specific dates.

Cash flow management is the owner’s early-warning system. It tells you whether the business can pay what is coming, whether customers are paying too slowly, and whether growth is creating more pressure than it solves.

This guide gives Singapore SME owners a simple dashboard to review weekly and monthly.

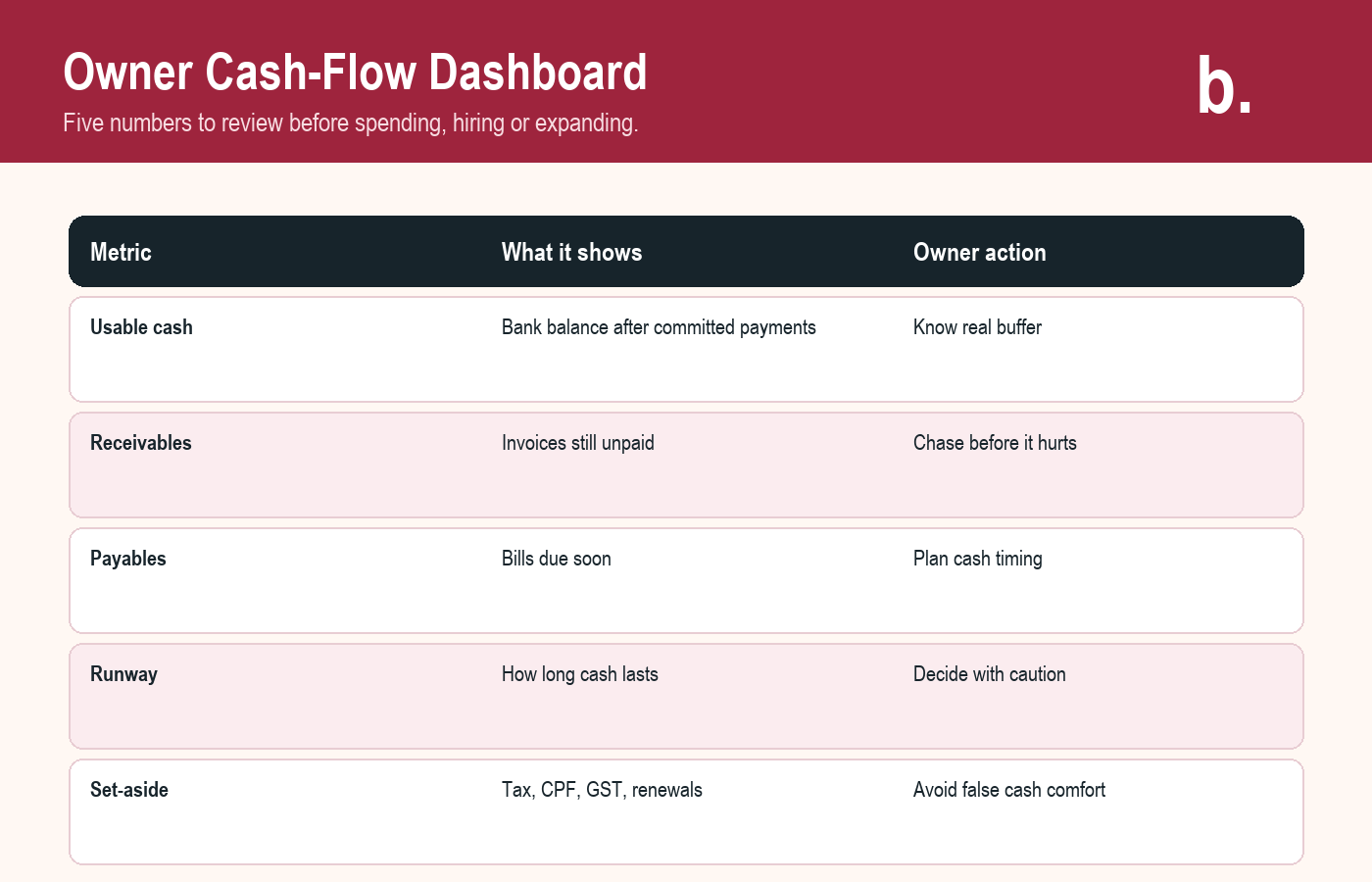

The cash-flow dashboard owners should review

You do not need a complicated finance dashboard to start. You need a short view that shows cash, timing and risk.

Dashboard item | What to track | Owner question |

|---|---|---|

Cash balance | Bank balance minus committed payments | How much usable cash do we really have? |

Receivables | Unpaid invoices by age | Who owes us money and how late is it? |

Payables | Supplier bills, rent, software, loans, CPF, tax | What must be paid in the next 30 days? |

Runway | Months the business can operate at current cash burn | How long can we survive if sales slow down? |

Tax and compliance set-aside | GST, corporate tax, CPF and payroll obligations | Are we spending money that belongs to future obligations? |

Why profitable businesses can still run out of cash

Profit is an accounting view. Cash flow is the timing of money entering and leaving the bank account. A business can be profitable on paper and still struggle if customers pay late, inventory is bought upfront, or expansion requires cash before revenue arrives.

- Invoices may be issued but unpaid.

- Stock, contractors or ad spend may be paid before customers pay you.

- GST, CPF, salary and tax obligations can arrive after cash has already been spent.

- Growth can increase working capital pressure.

Weekly cash-flow routine

A weekly review keeps the owner close to reality without turning finance into a full-day exercise.

- Check actual bank balance.

- List payments due in the next 14 and 30 days.

- Review overdue invoices and assign follow-up.

- Update expected incoming payments.

- Decide whether spending, hiring or purchases should wait.

Monthly management view

Once a month, step back from the bank account and review the pattern.

Receivable days

If customers are paying slower, the issue may be weak payment terms, unclear invoices or no follow-up rhythm.

Recurring commitments

Review rent, payroll, subscriptions, loans, retainers and insurance. Recurring costs are where small leaks become permanent.

Cash set-aside

Use a separate line or account for future tax, CPF, GST where relevant, and major renewals. Do not treat all bank balance as free cash.

Official and practical references

- IRAS: record keeping requirements

- SBO: invoice financing in Singapore

- SBO: bookkeeping for Singapore small businesses

The bottom line

Cash flow management is not just for finance teams. It is an owner habit. A simple weekly dashboard can prevent late surprises, weak collections and overconfident spending.

Frequently Asked Questions

What is cash flow management?

Cash flow management is the process of tracking money coming in, money going out and whether the business can meet upcoming obligations on time.

How often should SME owners review cash flow?

A weekly review is practical for most SMEs, with a deeper monthly review of receivables, payables, runway and recurring costs.

Is profit the same as cash flow?

No. Profit measures business performance over a period, while cash flow focuses on the timing of money entering and leaving the bank account.

What is the most important cash-flow metric?

For many SMEs, overdue receivables and upcoming payables are the first metrics to watch because they directly affect whether the business can pay bills.

Explore More Content

Table of Content