A business credit card can make monthly operations smoother, but it can also create messy spending if the controls are weak. For a small business owner, the useful question is not only which card gives the best reward. It is whether the card helps with cash flow, staff spending, receipts, travel, subscriptions, and accounting without encouraging unnecessary debt.

Business credit card options to compare

Option type

Best fit

What to verify before applying

DBS business cards

SMEs already using DBS banking or wanting local bank card support.

Card type, annual fee, rewards, interest, eligibility, and expense workflow.

UOB business cards

Companies that want an established local bank relationship and card programme.

Current card availability, credit limit policy, fees, and payment terms.

American Express business or corporate cards

Businesses that value travel, supplier payments, or corporate card controls.

Acceptance, membership fee, points value, spending controls, and settlement terms.

Citi commercial cards

Larger or growing companies that need corporate card and expense programme support.

Minimum requirements, programme setup, reporting, and employee card controls.

Standard Chartered business cards

Businesses comparing bank-backed card options with financing and banking products.

Current product availability, charges, rewards, and eligibility.

Aspire corporate cards

Digital-first SMEs that need virtual cards, spend limits, approvals, and receipt capture.

Whether it is credit, charge, debit, or prepaid in your setup, and how repayments work.

A useful business card should improve control, cash flow and bookkeeping, not just offer headline rewards.

How to choose a business credit card

Start from the spending pattern, not the rewards table. A cashback or points card is only valuable if the company can pay in full and keep the admin clean.

Cash flow: check billing cycle, due date, interest rate, and whether the business can pay in full.

Receipts: check whether receipts can be captured and matched to transactions easily.

Rewards: compare cashback, points, miles, and exclusions after fees.

Acceptance: check whether key suppliers accept the card and whether surcharges apply.

Accounting: check statement exports and integrations with your bookkeeping process.

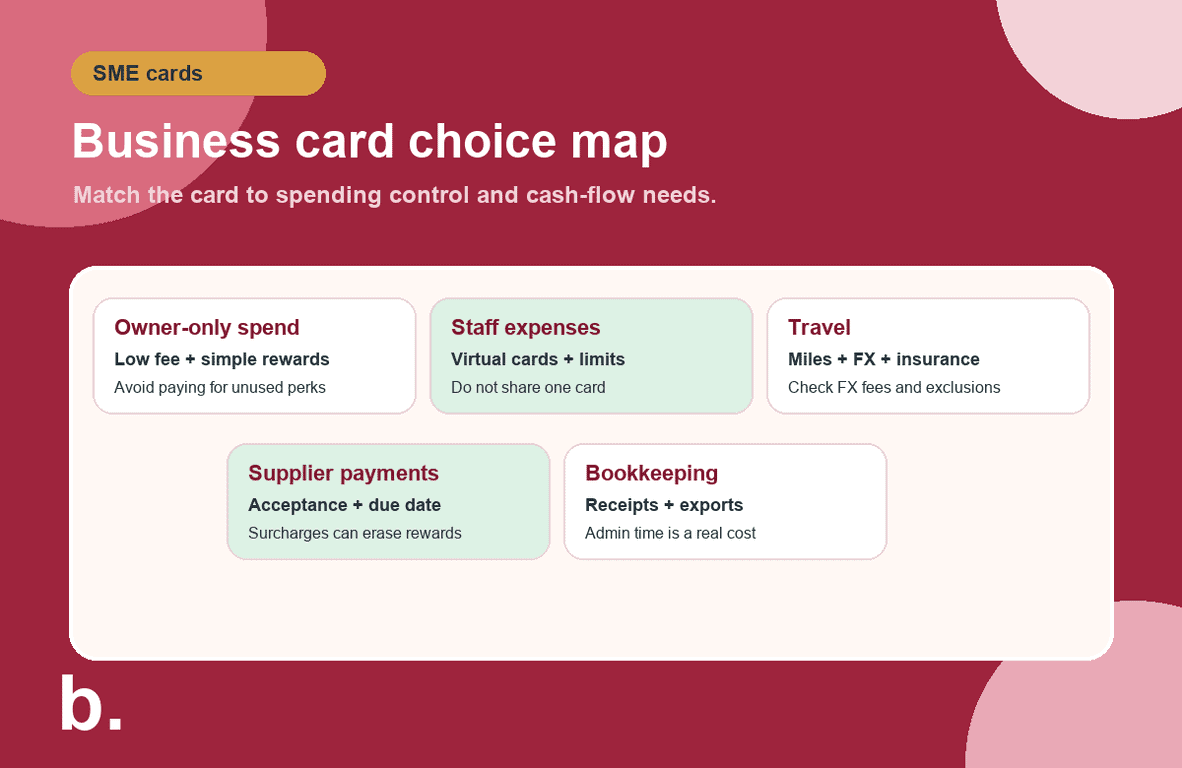

Decision table for SME owners

Business need

Card feature to prioritise

Watch-out

Owner-only monthly expenses

Simple rewards and clear statement

A high-fee card may not be worth it if spend is low.

Multiple staff buying online tools

Virtual cards, category limits, and approval rules

Shared card details create weak accountability.

Frequent travel

Miles, lounge benefits, FX terms, travel insurance

Benefits can be offset by FX fees and annual fees.

Supplier payments

Payment acceptance and working-capital timing

Supplier surcharges may erase reward value.

Accounting cleanup

Exports, receipt capture, and card-level reporting

Rewards are not helpful if bookkeeping becomes slower.

When a debit or spend card may be better

Not every business needs credit. If the main issue is staff spending control, a debit card, prepaid card, or fintech spend card may be cleaner than a revolving credit line.

Use a credit card when short billing-cycle cash flow and rewards are valuable.

Use a debit or spend card when the priority is control, no interest risk, and clean expense tracking.

Use virtual cards when staff need separate limits for ads, software, travel, or supplier accounts.

What is the best business credit card in Singapore?

The best card depends on spending pattern. Compare fees, rewards, credit terms, employee controls, receipt capture, and whether your main suppliers accept card payments.

Can a new company get a business credit card?

Some providers may support young companies, but approval depends on eligibility, business profile, credit review, and the provider’s current policy.

Is a business debit card better than a credit card?

A debit or spend card can be better when control and no-interest spending matter more than a credit line or rewards.

Should I use a personal credit card for business expenses?

It is cleaner to separate business and personal spending. A dedicated business card makes bookkeeping, receipts, and tax records easier to manage.