A founder may apply for a business facility, company card, or rental agreement and suddenly realise that personal credit history still matters. In Singapore, credit reports help lenders assess how reliably a borrower has handled past credit. For small business owners, this is relevant because the company may be young, thinly capitalised, or dependent on the owner as guarantor. Understanding your credit score helps you spot issues before a financing conversation starts.

What a credit score means in Singapore

A credit score is a summary of credit risk based on credit information held by the bureau. It is not a promise that a loan will be approved. Banks and finance companies still consider income, debt servicing, collateral, business performance, and their own credit policy.

Score range

Grade

Risk band

Probability of default

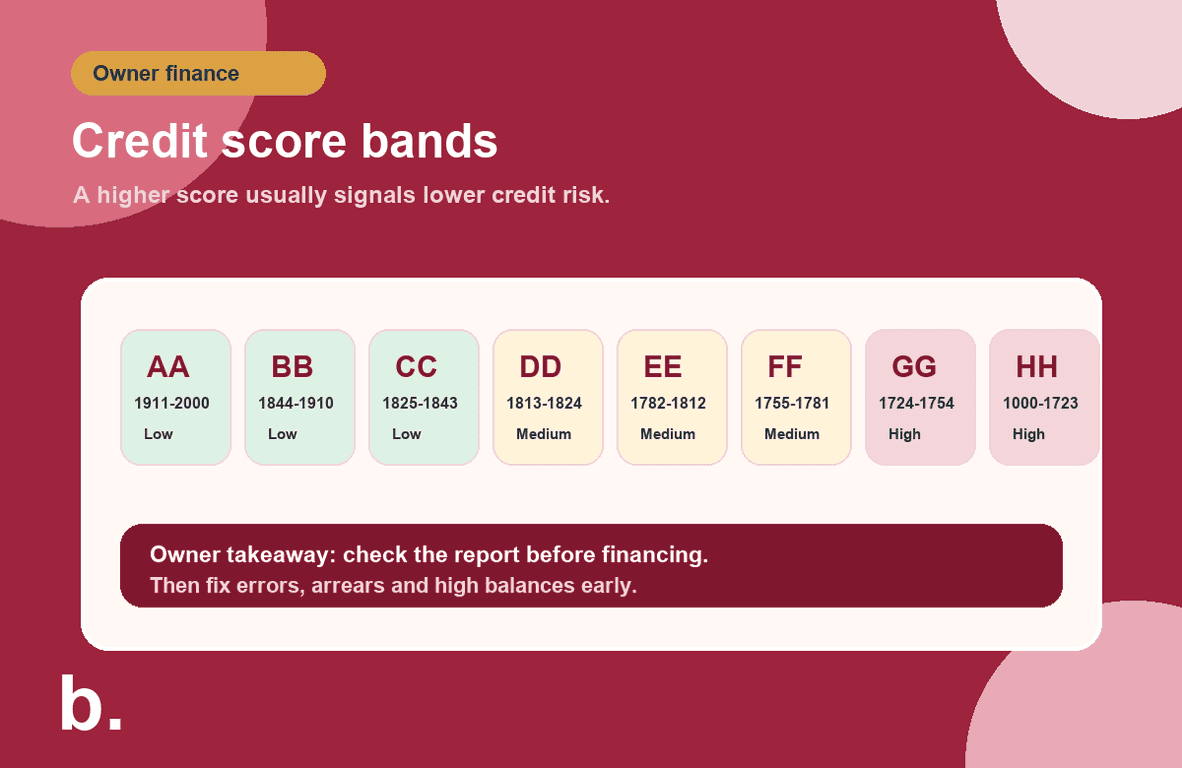

1911 – 2000

AA

Low risk

< 0.27%

1844 – 1910

BB

Low risk

0.27% – 0.67%

1825 – 1843

CC

Low risk

0.67% – 0.88%

1813 – 1824

DD

Medium risk

0.88% – 1.03%

1782 – 1812

EE

Medium risk

1.03% – 1.58%

1755 – 1781

FF

Medium risk

1.58% – 2.28%

1724 – 1754

GG

High risk

2.28% – 3.48%

1000 – 1723

HH

High risk

> 3.48%

Credit score bands help business owners understand how lenders may read personal credit risk before financing.

Why business owners should care

Young companies may have little track record: lenders may pay more attention to the owner, director, or guarantor.

Personal and business cash flow can overlap: late personal repayments can make business financing harder to explain.

Credit cards and facilities depend on policy: a good score helps, but it does not replace income or business fundamentals.

Errors should be fixed early: checking the report before applying gives you time to clarify or correct problems.

What usually helps or hurts your score

Behaviour

Likely effect

Owner takeaway

Paying credit cards and loans on time

Helps

Automate minimum payments if cash flow is irregular.

Repeated late payments or defaults

Hurts

Prioritise arrears before applying for new credit.

Using a high portion of available credit

Can hurt

Reduce balances before major financing applications.

Many credit applications in a short period

Can hurt

Shortlist lenders before applying everywhere.

Checking your own credit report

Useful for monitoring

Review details and dispute inaccuracies where needed.

How to improve your credit position

Credit improvement is usually a consistency exercise. The goal is to show that repayments are predictable and that existing credit is under control.

Pay bills, credit cards, and loan instalments by the due date.

Reduce revolving credit balances where possible.

Avoid applying for multiple cards or loans at the same time.

Check your report before an important loan or facility application.

Keep business and personal cash flow records clean so lenders can understand the story.

Official pages to check

This guide was reviewed on 28 June 2026. Check current details with Credit Bureau Singapore and general borrowing guidance from MoneySense before making a financing decision.

Frequently Asked Questions

What is a good credit score in Singapore?

A higher score generally indicates lower credit risk. In the CBS score bands, AA and BB sit in the low-risk range, but lenders still assess income, debts, business performance, and their own policy.

Does my personal credit score affect my business loan?

It can, especially for small businesses, young companies, or facilities where the owner provides a personal guarantee.

How can I check my credit score in Singapore?

You can request a credit report from Credit Bureau Singapore. Check the official CBS website for current access methods, fees, and free-report conditions.

Can I improve my credit score quickly?

You can fix errors and pay overdue balances quickly, but a stronger credit profile usually takes consistent on-time repayment over time.