We make boring business stories sparkle.

Should Business Owners Take a Personal Loan in Singapore?

A practical guide for Singapore business owners considering a personal loan for cash flow, including risks, alternatives, bank vs licensed moneylender checks, and when borrowing makes sense.

A personal loan can look like the fastest way to patch a business cash-flow gap. The application is in your own name, the money can be disbursed quickly, and you may not need to prepare a full business loan package.

That speed is also the danger. If you use a personal loan for business, the debt remains your personal obligation even if the business does not recover. For a Singapore business owner, the real question is not just “Can I get the loan?” It is “Should I put my personal balance sheet behind this problem?”

This guide explains what a personal loan is, how it works, how it compares with business financing, and how to think before borrowing from a bank or licensed moneylender in Singapore.

What is a personal loan?

A personal loan is money borrowed by an individual, usually without pledging a specific asset as collateral. In Singapore, bank personal loans are commonly unsecured instalment loans approved based on your personal income, credit profile, debt obligations, and the lender’s policy.

The lender disburses a lump sum to you. You repay it over a fixed period through monthly instalments made up of principal, interest, and any applicable fees. The loan contract is between you and the lender, not your company.

How a personal loan works in practice

- You apply using your personal details, income documents, identity details, and credit information.

- The lender assesses your ability to repay and may check your credit bureau record.

- If approved, you receive a loan amount, tenure, interest rate, fees, and repayment schedule.

- You receive the money and start monthly repayments.

- If you miss payments, late fees, interest, collection action, and credit score damage may follow.

For business owners, especially sole proprietors and directors of small companies, the money may be used to support operations. But legally and financially, it is still your personal debt unless the facility is clearly a business loan taken by the company.

Should a business owner use a personal loan for business?

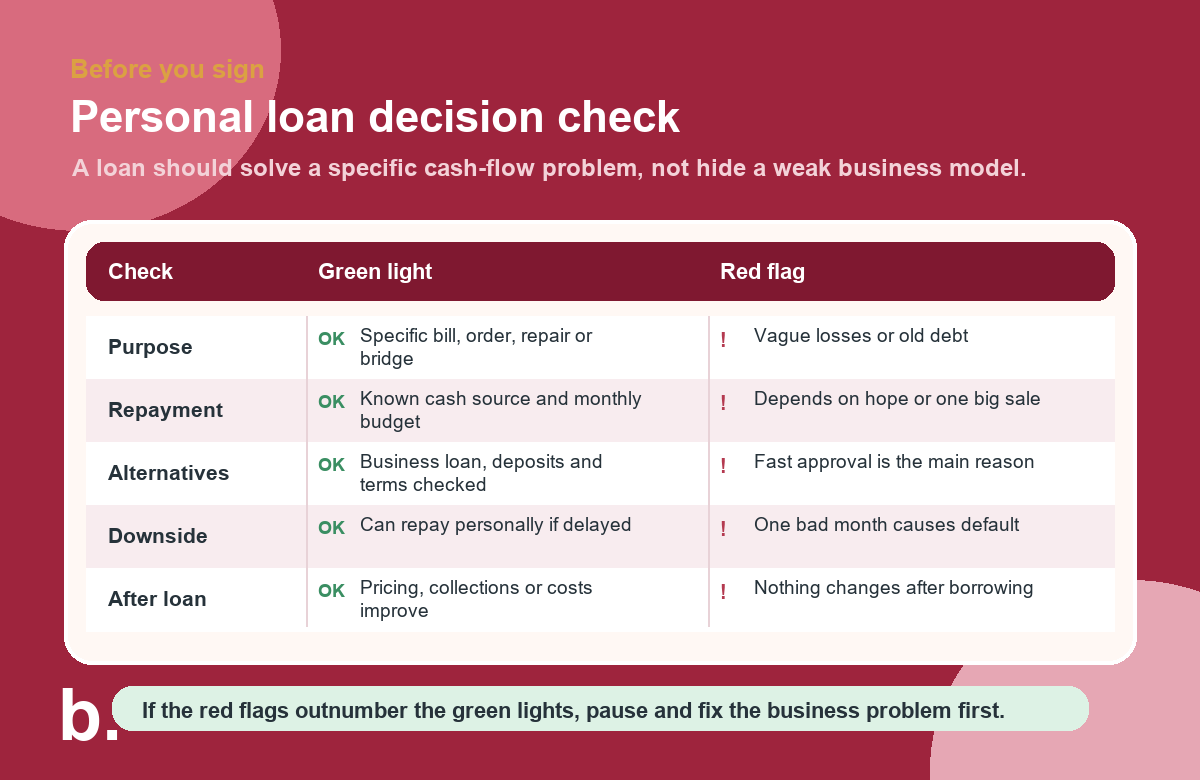

Sometimes, but only after a hard check. A personal loan may be reasonable when the amount is small, the repayment source is clear, and the business problem is temporary. It is dangerous when it is used to delay a deeper business problem.

The cleaner rule is this: use business financing for business needs whenever the business can qualify. Use a personal loan only when the business case is strong, the gap is short term, and you can still repay from personal income if the business plan fails.

Question | Good answer | Warning sign |

|---|---|---|

What is the loan for? | A specific short-term gap, stock purchase, equipment repair, or receivable delay | General losses, vague “working capital”, or covering unpaid old debt |

How will it be repaid? | Known cash inflow, salary, contract payment, or controlled monthly budget | Hope that sales will improve without signed orders or proof |

Can the business survive without it? | Yes, but the loan prevents disruption or captures a profitable opportunity | No, the business cannot meet basic obligations without more debt |

Can you repay personally? | Yes, even if the business recovery is delayed | No, repayment depends entirely on a risky turnaround |

Have alternatives been checked? | Supplier terms, customer deposits, grants, business loan, overdraft, invoice financing | No comparison; lender speed is the main reason |

Personal loan vs business loan: key differences

A personal loan and a business loan may both put cash in your account, but they solve different problems and create different risks.

Financing type | Borrower | Best suited for | Main risk |

|---|---|---|---|

Personal loan | Individual owner | Small, urgent, personal-backed cash needs | Owner is personally liable even if business fails |

Business term loan | Company or business entity | Working capital, expansion, equipment, planned cash needs | Approval may require financial records, director guarantee, and longer processing |

Overdraft or credit line | Business or individual, depending on facility | Short-term uneven cash flow | Easy to keep rolling debt instead of repaying it |

Invoice financing | Business | Waiting for customers to pay approved invoices | Cost, customer concentration, and invoice eligibility |

Trade loan | Business | Import, export, inventory, supplier payment cycles | Useful only when tied to real trade activity |

Business credit card | Business or owner, depending on card | Short expense timing gaps and controls | High interest if balances are rolled |

Government-assisted SME financing | Eligible business | Working capital, trade, fixed assets, projects, green loans, venture debt, M&A | Eligibility and approval are still assessed by participating financial institutions |

Enterprise Singapore’s Enterprise Financing Scheme covers several business financing needs, including SME working capital loans, fixed asset loans, trade loans, project loans and other facilities. This does not mean every SME will qualify, but it is worth checking before converting a business problem into personal debt.

If you are still setting up your banking and finance foundation, read our guides to business bank accounts in Singapore, business credit cards, and credit score in Singapore.

When a personal loan may make sense

A personal loan is most defensible when it is used for a contained, measurable problem with a clear repayment path.

1. The amount is modest and temporary

For example, a small service business has confirmed invoices due in 30 to 60 days, but needs to cover payroll or a supplier deposit this month. If the repayment source is highly likely and documented, the loan may be a bridge.

2. The loan unlocks profitable work

A cafe may need a critical equipment repair to continue trading. A contractor may need materials for a signed job with a deposit already received. In these cases, the loan supports revenue that is reasonably visible.

3. Business financing is too slow for a real emergency

Some bank business loans take time because the lender wants financial statements, bank records, tax documents, and internal approval. If delay would cause a bigger loss, a personal loan may be considered as a stopgap, provided the owner has a repayment fallback.

4. You have separated the business decision from the emotional pressure

Borrowing under panic usually leads to bad terms. A good borrowing decision can be explained on one page: amount needed, purpose, repayment source, downside scenario, and alternatives checked.

Bad reasons to take a personal loan

Some reasons feel urgent but are structurally weak. These are usually signs to pause, negotiate, cut costs, restructure, or seek professional help instead of adding personal debt.

- To cover repeated monthly losses. If the business loses money every month, a personal loan may only buy time while increasing personal risk.

- To pay another high-interest loan. Debt consolidation can make sense only if it reduces total cost and has a strict repayment plan. Otherwise, it becomes a debt spiral.

- To avoid a difficult conversation. It may be better to negotiate with suppliers, landlords, lenders, staff, or customers than quietly borrow personally.

- To fund an untested idea. New marketing, inventory, expansion, or renovation should have numbers behind it, not optimism.

- To protect pride. Borrowing to avoid admitting that a business model is not working is one of the most expensive mistakes an owner can make.

- To mix shareholder issues with personal rescue money. If there are partners, document whether the money is a director loan, shareholder loan, capital injection, or personal expense. Do not assume everyone will remember it the same way later.

Pros and cons of using a personal loan for business

Pros

- Fast access. Personal loans can be quicker than full business loan applications.

- Simple documents. Banks may focus more on your personal income and credit profile than your company accounts.

- Flexible use. The cash is not always tied to a specific invoice, asset, or trade transaction.

- Useful for very small gaps. For micro-businesses, a small personal loan may be easier than a formal SME facility.

Cons and dangers

- Personal liability. You owe the money personally even if the business fails.

- Credit score damage. Missed repayments can hurt future personal and business financing.

- Higher cost than secured lending. Unsecured loans usually cost more than loans backed by strong collateral or business cash flow.

- False confidence. Fresh cash can hide weak margins, poor pricing, slow collections, or unsustainable expenses.

- Family stress. Personal repayments compete with mortgage, rent, family support, insurance, and emergency savings.

- Accounting confusion. If money goes from your personal account into the business, record it properly as a loan, capital injection, or reimbursable expense with your accountant.

The thought process before borrowing

Before taking any loan, write the answer to these questions. If you cannot answer them clearly, you are not ready to borrow.

- What exact problem does this loan solve? Name the bill, gap, purchase, or opportunity.

- Is the problem temporary or structural? Temporary cash timing can be financed. Broken margins usually need operational change.

- What is the total repayment amount? Look beyond the headline rate. Include processing fees, late fees, annual fees, and effective interest rate where available.

- What is the monthly instalment? Compare it with personal take-home income and business cash-flow forecasts.

- What happens if sales are 30% lower than expected? If one bad month causes default, the loan is too tight.

- What cheaper alternatives exist? Customer deposits, staged delivery, supplier credit, grant timing, expense cuts, invoice financing, or a business loan may be better.

- What must change after borrowing? A loan should come with action: repricing, collection process, cost cuts, new sales discipline, or contract terms.

Bank personal loan vs licensed moneylender

For most business owners, a bank should be checked before a licensed moneylender because bank pricing and repayment structures are usually more suitable for longer repayment periods. A licensed moneylender may be faster or more accessible, but the cost and risk can be much higher.

Area | Bank personal loan | Licensed moneylender loan |

|---|---|---|

Regulator or official checker | Banking and consumer credit rules; check lender’s official bank site | Check the Registry of Moneylenders list before dealing with anyone |

Typical borrower check | Income, credit bureau record, debt obligations, employment or self-employed income proof | Identity, income documents, loan application, and required face-to-face verification |

Cost structure | Interest, processing fees, late fees, early repayment terms may apply | Interest, late interest, administrative fee, late fees, and legal costs are capped by law but can still be expensive |

Speed | Often fast for eligible applicants, but depends on bank and documents | Can be fast, but should never be fully online or based only on SMS or phone approval |

Best use case | Borrower with stable income and credit profile who needs a structured instalment loan | Last resort for small, short-term borrowing after safer options are checked |

Main danger | Overborrowing because approval feels easy | High monthly cost, scams, aggressive collection, and borrowing under pressure |

What to check before applying to a bank

- Compare the effective interest rate, not just the advertised flat rate.

- Check processing fees, late payment fees, early repayment fees, and whether insurance or add-ons are optional.

- Prepare NRIC or identification, income documents, CPF contribution history where relevant, Notice of Assessment, bank statements, and self-employed income proof if applicable.

- Check whether the lender accepts your income type. Directors and self-employed owners may need more documents than salaried employees.

- Confirm the monthly instalment fits your personal budget even if the business does not improve immediately.

What to check before dealing with a licensed moneylender

Use the Registry of Moneylenders list to verify the lender’s name, approved place of business, and official website before you contact them. Do not rely on an SMS, WhatsApp message, social media account, or website that merely claims to represent a licensed moneylender.

MinLaw’s borrower FAQ states that licensed moneylenders must explain the loan terms in a language you understand and provide a copy of the loan contract. It also warns borrowers to understand the repayment schedule, interest rate, and fees before signing.

- Do not pay “GST”, processing fees, deposits, or any upfront transfer before loan disbursement.

- Do not give anyone your Singpass password, internet banking password, ATM card, NRIC card, passport, work permit, or other personal documents to hold.

- Do not sign a blank or incomplete loan contract.

- Do not proceed if the loan is granted fully by phone, SMS, email, or online without proper checks.

- Do not respond to loan advertisements by SMS or WhatsApp. Licensed moneylenders are not allowed to solicit loans through such channels.

- Meet only at the approved place of business shown on the official Registry list.

Licensed moneylender limits and charges

MinLaw’s current borrower FAQ states that, for unsecured loans from licensed moneylenders, Singapore citizens and permanent residents with annual income below S$10,000 may borrow up to S$3,000 in total across all moneylenders. Those with annual income of at least S$10,000 but less than S$20,000 may also borrow up to S$3,000. Those with annual income of at least S$20,000 may borrow up to six times monthly income.

For foreigners residing in Singapore, the stated unsecured borrowing limit is S$500 if annual income is below S$10,000, S$3,000 if annual income is at least S$10,000 but less than S$20,000, and six times monthly income if annual income is at least S$20,000.

Licensed moneylenders may charge up to 4% interest per month, and up to 4% late interest per month on overdue amounts. They may also charge a late fee of up to S$60 for each month of late repayment, an administrative fee of up to 10% of the principal when the loan is granted, and court-ordered legal costs for successful recovery claims. MinLaw also states that total charges made up of interest, late interest, upfront administrative fee and late fees cannot exceed an amount equal to the loan principal.

Those caps do not make borrowing cheap. A loan that is legal can still be a poor business decision.

A simple pre-loan checklist for business owners

Use this checklist before signing any loan document.

- Business case: I know exactly what this loan funds and how it helps revenue, continuity, or cash flow.

- Repayment source: I can name the cash source for every instalment.

- Downside plan: I can still repay if the business outcome is delayed or weaker than expected.

- Cost comparison: I compared total repayment amount, effective interest, fees, and late charges.

- Alternatives: I checked business loans, supplier terms, customer deposits, invoice financing, grants, cost cuts, and partner capital.

- Documentation: If the money goes into the business, I will record it properly in the accounts.

- No pressure: I am not borrowing because someone rushed me, threatened me, or promised instant approval by message.

- No secrets: If the loan affects family finances or business partners, the right people know the risk.

What to do if the business is already under stress

If the business cannot pay rent, payroll, suppliers, taxes, or existing loans, pause before taking more personal debt. Borrowing may still be part of the solution, but it should sit inside a recovery plan.

- Prepare a 13-week cash-flow forecast.

- Separate urgent, important, and negotiable payments.

- Call key suppliers early and ask for structured repayment terms.

- Invoice faster and chase receivables more firmly.

- Review pricing, gross margin, slow-moving stock, and unprofitable customers.

- Cut recurring expenses that do not protect sales or operations.

- Speak to your accountant if director loans, shareholder loans, tax arrears, or insolvency risk are involved.

- Contact Credit Counselling Singapore or another suitable support organisation if personal debt is already becoming unmanageable.

A loan is useful only if the business after the loan is stronger than the business before the loan. If nothing changes, the loan may simply move the crisis from the company to the owner.

Frequently Asked Questions

Can I use a personal loan for my business in Singapore?

You may be able to use a personal loan for business needs, depending on the lender’s terms, but the debt remains your personal obligation. Business owners should compare business financing first and borrow personally only when the repayment plan is clear.

Is a personal loan better than a business loan?

Usually no. A business loan is cleaner when the money is for business operations because the facility is assessed around the business need. A personal loan may be faster, but it transfers more risk to the owner personally.

Should I borrow from a licensed moneylender for business cash flow?

Treat licensed moneylender loans as a last resort for small, short-term needs. Always verify the lender on the Registry of Moneylenders list, check the full cost, avoid upfront payments, and do not borrow if repayment depends on hope.

What is the biggest danger of using personal loans for business?

The biggest danger is using personal debt to cover a business model that is structurally losing money. If sales, pricing, collections, or costs do not improve, the owner may end up with both a weak business and personal debt.

What should I prepare before applying for a personal loan as a business owner?

Prepare identity documents, income proof, recent bank statements, tax documents such as Notice of Assessment where relevant, and a personal budget showing that you can afford the instalments. Self-employed owners and directors may need more documents than salaried employees.

The bottom line

A personal loan can help a Singapore business owner through a short, specific cash-flow gap. It should not be the first answer to recurring losses, unclear strategy, or pressure from overdue bills.

Before borrowing, compare business financing, check the total repayment amount, and stress-test the instalment against your personal budget. If you use a personal loan, keep the amount modest, document the money properly, and make sure the business changes that caused the cash-flow problem are actually fixed.

In hard times, the best loan is not the fastest one. It is the one attached to a realistic recovery plan.

Explore More Content

Table of Content