We make boring business stories sparkle.

How to Read Your Company Financial Statements Without Being an Accountant

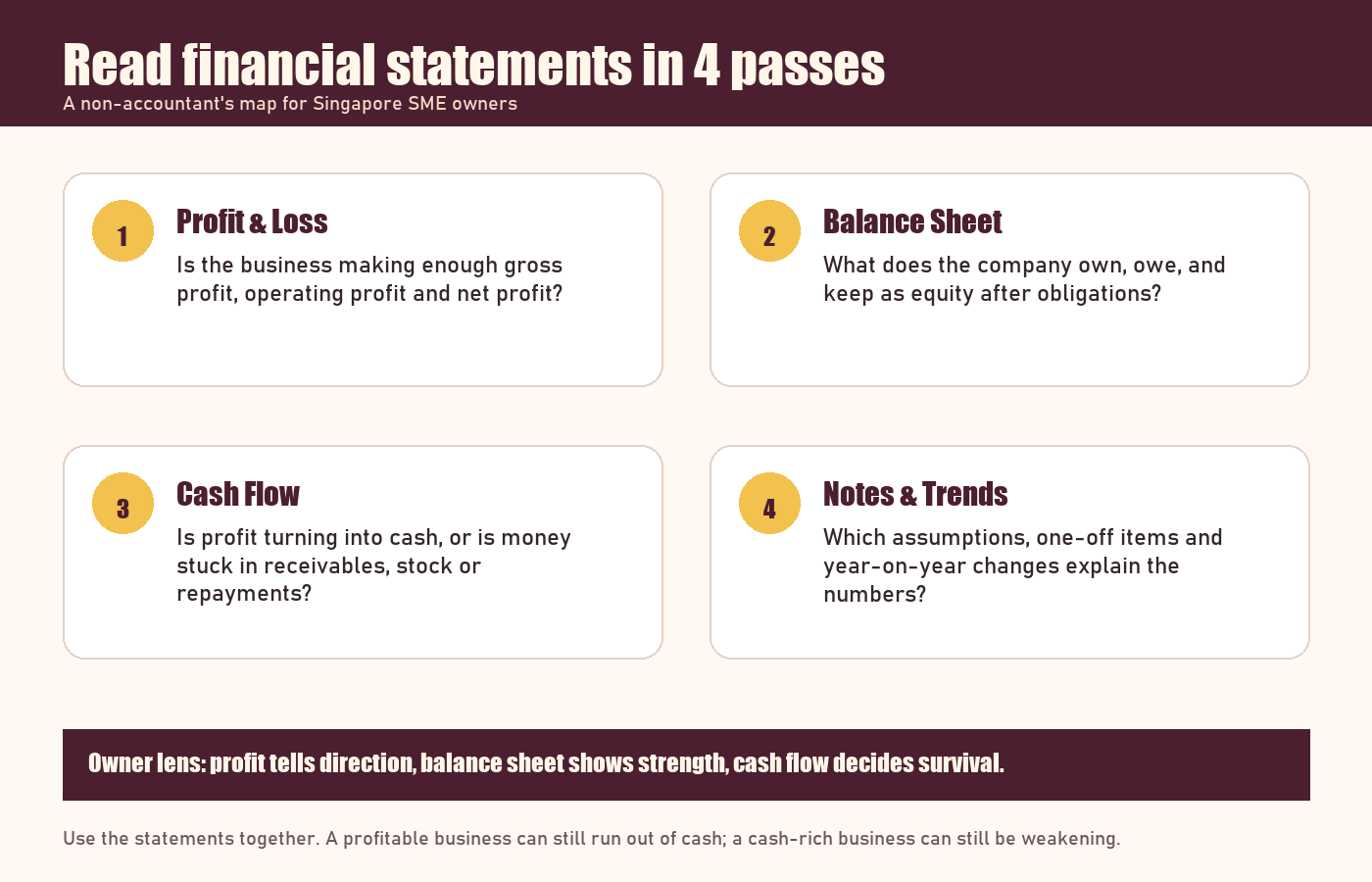

A plain-English guide for Singapore SME owners to read P&L, balance sheet and cash flow statements without being an accountant.

The owner of a small agency looks at the year-end accounts and sees three documents from the accountant: a profit and loss statement, a balance sheet and a cash flow statement.

The business made a profit. That should feel good. But the bank balance is tight, two customers are paying late, and the owner is not sure whether the company can hire another designer.

This is where financial statements become useful. They are not just documents for accountants, banks or tax filing. Read properly, they show whether your business is earning enough, staying solvent, collecting cash and building resilience.

This guide explains how Singapore business owners can read company financial statements without becoming accountants.

Why Business Owners Should Read Financial Statements

You do not need to prepare the accounts yourself. But you should understand what the statements are telling you.

Financial statements help you answer practical owner questions:

- Are sales growing in a healthy way?

- Is gross profit enough to cover overheads?

- Are customers paying too slowly?

- Is too much cash stuck in inventory or deposits?

- Can the company afford a hire, loan repayment or expansion?

- Are dividends or owner withdrawals sensible?

IRAS also expects companies to maintain proper transaction records and retain source documents, accounting records, schedules, bank statements and other related business records for at least 5 years from the relevant Year of Assessment. Good statements are easier to trust when the underlying records are clean.

The Four Documents You Should Know

Most SME owners can start with four parts of the accounts.

Statement | Plain-English question | Owner takeaway |

|---|---|---|

Profit and loss statement | Did we make money from operations? | Shows revenue, costs, expenses and profit. |

Balance sheet | What do we own and owe? | Shows assets, liabilities and equity at a point in time. |

Cash flow statement | Where did cash actually move? | Shows whether profit is turning into cash. |

Notes to accounts | What details explain the numbers? | Shows policies, breakdowns, commitments and context. |

Start With the Profit and Loss Statement

The profit and loss statement, often called P&L, shows business performance over a period. It usually covers a month, quarter or financial year.

The basic flow is:

Line item | What it means | Simple example |

|---|---|---|

Revenue | Sales earned before expenses. | $500,000 |

Cost of sales | Direct cost of delivering the product or service. | ($220,000) |

Gross profit | Revenue minus direct costs. | $280,000 |

Operating expenses | Rent, payroll, software, marketing, admin and other overheads. | ($210,000) |

Net profit before tax | Profit before corporate income tax. | $70,000 |

Gross Profit Is Your First Health Check

Gross profit tells you whether your pricing and delivery model work.

If revenue grows but gross profit margin falls, your business may be buying growth at a bad price. Common causes include discounts, higher supplier costs, inefficient fulfilment or underpriced projects.

A simple gross profit margin formula is:

Gross profit margin = Gross profit / Revenue x 100%

Using the example above:

$280,000 / $500,000 x 100% = 56%

Net Profit Is Not the Same as Cash

Net profit tells you whether the company was profitable on paper. It does not tell you whether the money is already in the bank.

A business can show profit while still struggling for cash because customers have not paid, stock was purchased upfront, loan repayments are due, or tax payments are coming.

Then Read the Balance Sheet

The balance sheet is a snapshot of the company at a specific date.

It follows this basic structure:

Assets = Liabilities + Equity

Assets are what the company controls. Liabilities are what the company owes. Equity is the owner or shareholder value left after liabilities.

Balance sheet item | Examples | What owners should ask |

|---|---|---|

Current assets | Cash, receivables, inventory | Can these become cash soon? |

Non-current assets | Equipment, vehicles, long-term investments | Are these assets productive? |

Current liabilities | Supplier bills, tax payable, short-term loans | What must be paid soon? |

Non-current liabilities | Long-term loans and obligations | Can the business support the repayment? |

Equity | Share capital and retained earnings | Is the business building value over time? |

Watch Receivables Closely

Receivables are amounts customers owe you. High receivables can make profit look strong while cash remains weak.

If receivables keep growing faster than revenue, ask:

- Are customers paying later than agreed?

- Are invoices being sent too slowly?

- Are we accepting too much credit risk?

- Do we need deposits, milestone billing or stricter payment terms?

Watch Short-Term Obligations

Current liabilities matter because they need to be paid soon. A company with high sales but weak cash can still get into trouble if supplier bills, payroll, GST, CPF, tax or loan payments are due before customers pay.

Use Cash Flow to Check Reality

The cash flow statement explains how cash moved in and out of the company.

It normally separates cash into operating, investing and financing activities.

Cash flow section | What it shows | Owner interpretation |

|---|---|---|

Operating cash flow | Cash from day-to-day business activity. | Should be healthy over time for a sustainable business. |

Investing cash flow | Cash used for assets or received from asset sales. | Negative may be fine if the company is investing productively. |

Financing cash flow | Cash from loans, repayments, share capital or dividends. | Shows whether growth is funded by operations, debt or owners. |

The strongest businesses usually generate positive operating cash flow consistently. If net profit is positive but operating cash flow is often negative, investigate quickly.

Five Ratios That Are Useful Without Being Too Technical

Ratios help you compare numbers across months or years. You do not need dozens of ratios. Start with these five.

Ratio | Formula | What it tells you |

|---|---|---|

Gross profit margin | Gross profit / Revenue | Whether pricing and direct costs work. |

Net profit margin | Net profit / Revenue | How much profit remains after expenses. |

Current ratio | Current assets / Current liabilities | Short-term ability to meet obligations. |

Receivable days | Trade receivables / Revenue x 365 | How long customers take to pay on average. |

Operating cash conversion | Operating cash flow / Net profit | Whether accounting profit is turning into cash. |

Do not treat ratios as magic pass-or-fail rules. Compare them against your own past performance, your payment terms and your industry reality.

A Simple Example: Profit Looks Good, Cash Looks Tight

Imagine a Singapore service business with these year-end numbers:

Item | Amount | Owner reading |

|---|---|---|

Revenue | $500,000 | Sales are meaningful. |

Net profit before tax | $70,000 | The company is profitable on paper. |

Trade receivables | $110,000 | A lot of sales are still unpaid. |

Cash balance | $35,000 | Cash buffer may be thin. |

Current liabilities | $95,000 | Near-term obligations are significant. |

The owner should not only celebrate the $70,000 profit. The bigger question is whether customers will pay fast enough to cover obligations.

Receivable days can give a useful warning:

$110,000 / $500,000 x 365 = about 80 days

If customer terms are supposed to be 30 days, that is a collection problem. The financial statements are pointing to an operational fix, not just an accounting observation.

Red Flags to Discuss With Your Accountant

Use these signs as prompts for a proper conversation.

- Revenue grows but gross profit margin keeps falling.

- Net profit is positive but operating cash flow is negative.

- Receivables grow faster than sales.

- Inventory grows but sales do not follow.

- Current liabilities are rising faster than current assets.

- Director loans or owner withdrawals are unclear.

- Tax, CPF, GST or supplier payables are repeatedly delayed.

- One large customer accounts for too much revenue or receivables.

Questions to Ask Before Making a Big Decision

Before hiring, borrowing, opening another outlet or paying dividends, review the statements with these questions.

- Is profit recurring, or was it caused by a one-off project?

- Can the current cash balance cover the next 3 months of obligations?

- Are customers paying within agreed terms?

- What happens if sales fall by 20% for one quarter?

- Which expenses are fixed even if revenue drops?

- Does the company have enough working capital for growth?

- Will the decision create new tax, payroll, financing or compliance obligations?

How to Build the Habit

Do not wait until year end. A monthly review is more useful than a perfect report that arrives too late.

A practical rhythm is:

- Review P&L every month for revenue, gross profit and overhead movement.

- Review receivables weekly if customers pay on credit.

- Review cash flow before committing to hiring, large purchases or dividends.

- Review the balance sheet quarterly for loans, inventory, tax payable and equity.

- Ask your accountant to explain unusual movements in plain English.

Final Thought

Financial statements are not there to make small business owners feel less capable. They are there to make the business visible.

When you know how to read the P&L, balance sheet and cash flow together, you stop managing only by bank balance or gut feel. You can see where profit is coming from, where cash is trapped, and whether the company is becoming stronger.

Frequently Asked Questions

What are the main financial statements a business owner should read?

Start with the profit and loss statement, balance sheet and cash flow statement. The notes to accounts are also useful because they explain accounting policies, breakdowns and unusual items.

Is profit the same as cash in the bank?

No. Profit is an accounting measure. Cash can be lower because customers have not paid, inventory was purchased, loan repayments were made, or tax and other obligations are due.

How often should SME owners review financial statements?

A monthly review is a practical starting point. Receivables and cash flow may need weekly attention if the business gives credit terms or has tight working capital.

What is the most important ratio for a small business owner?

There is no single ratio for every business. Gross profit margin, current ratio, receivable days and operating cash conversion are useful because they connect pricing, liquidity, collections and cash reality.

Do Singapore companies need to keep accounting records?

Yes. IRAS states that companies must maintain proper records of financial transactions and retain source documents, accounting records, schedules, bank statements and related records for at least 5 years from the relevant Year of Assessment.

Sources Checked

- IRAS record keeping requirements

- IRAS basic guide to corporate income tax for companies

- SBO guide to tax-deductible business expenses

Explore More Content

Table of Content