We make boring business stories sparkle.

Singapore Corporate Income Tax: How to Understand and Calculate It

A practical guide for Singapore business owners to understand corporate income tax, calculate examples and use SBO's corporate income tax calculator.

It is late at night, the shop is closed, and the founder finally opens the profit and loss report. The business made $120,000 profit for the year. For one second, that feels like a win.

Then the tax question appears: “Does this mean I owe 17% of $120,000 to IRAS?”

That is where many Singapore business owners get anxious. The headline corporate income tax rate is simple, but the actual computation is not just revenue multiplied by 17%, or even accounting profit multiplied by 17%. You need to understand chargeable income, tax adjustments, exemption schemes, rebates and set-offs.

This guide explains Singapore corporate income tax in plain English, shows worked examples, and links the numbers to SBO’s Corporate Income Tax Calculator so you can test your own figures.

Important: This is an educational guide, not tax advice. Check the latest IRAS guidance or speak to a qualified tax adviser before filing.

What Singapore Corporate Income Tax Is Based On

IRAS states that companies are taxed at a flat corporate income tax rate of 17% of chargeable income. This applies to both local and foreign companies.

The key phrase is chargeable income. It is not the same as sales, cash in the bank, or automatically the same as accounting profit.

Term | What it means | Common mistake |

|---|---|---|

Revenue | Money earned from sales before expenses. | Using revenue to estimate tax. |

Accounting profit | Profit shown in your accounts after expenses. | Assuming every accounting expense is deductible. |

Chargeable income | Income after tax adjustments, reliefs and allowances. | Forgetting add-backs, capital allowances or exemption schemes. |

Tax payable | Tax after applying the 17% rate and relevant rebates or set-offs. | Ignoring current YA rebate rules or treating estimates as final assessments. |

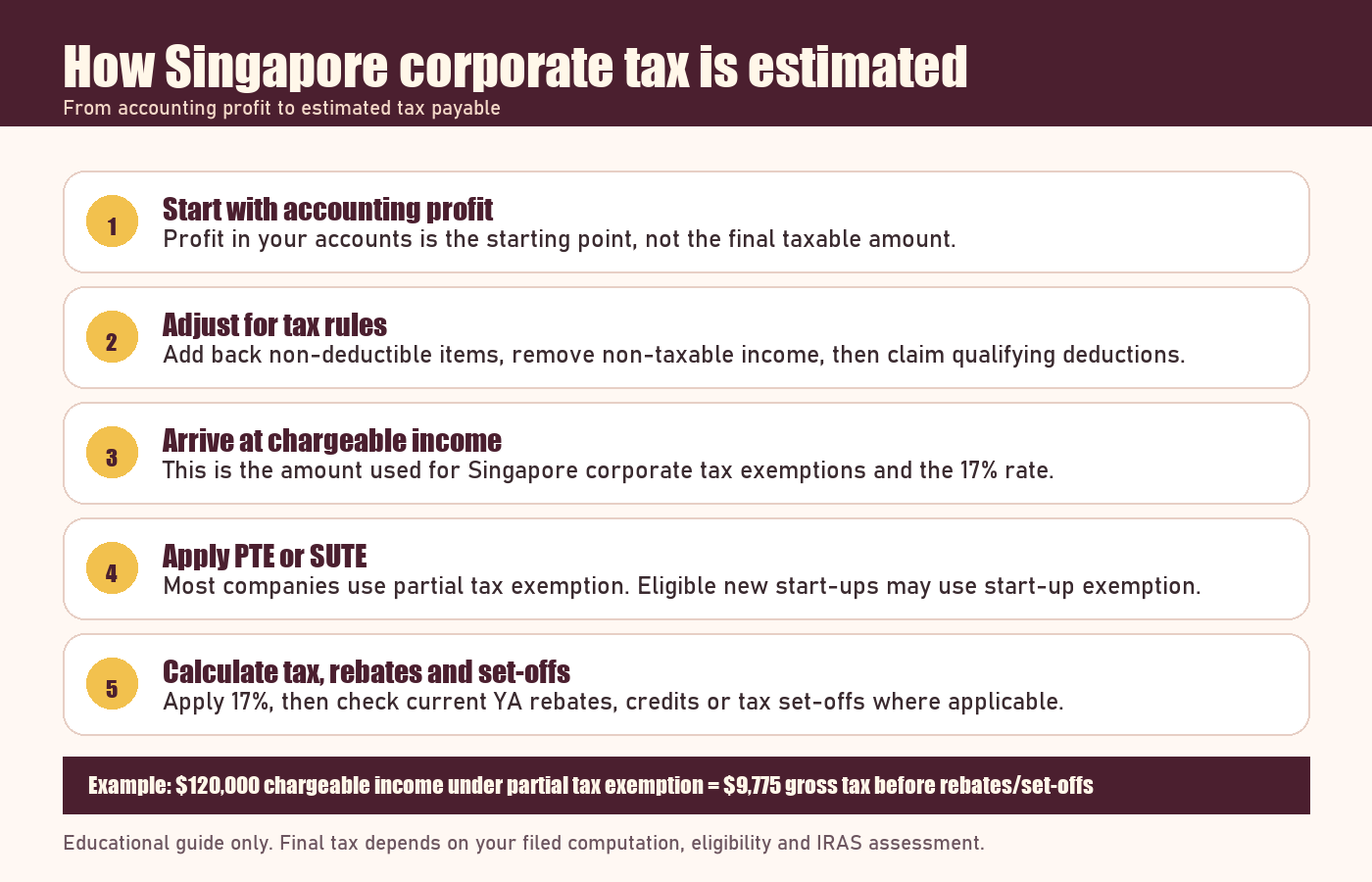

The Basic Corporate Tax Formula

A practical way to think about the flow is:

Step | Calculation movement | Why it matters |

|---|---|---|

1 | Start with accounting profit | Your financial accounts provide the base number. |

2 | Add back non-deductible expenses | Some expenses are real accounting costs but not tax-deductible. |

3 | Remove non-taxable income | Not every accounting income item is taxable in the same way. |

4 | Claim qualifying deductions and allowances | This can include allowable business expenses, capital allowances and other permitted claims. |

5 | Arrive at chargeable income | This is the number used for tax exemption schemes and the 17% rate. |

6 | Apply exemption, tax rate and set-offs | You estimate tax payable before IRAS issues the final assessment. |

Worked Example: A Company With $120,000 Chargeable Income

Assume a normal Singapore company has already made the correct tax adjustments and arrives at $120,000 of normal chargeable income.

For YA 2020 onwards, the partial tax exemption scheme generally exempts:

- 75% of the first $10,000 of normal chargeable income; and

- 50% of the next $190,000 of normal chargeable income.

Here is how the $120,000 example works before rebates and set-offs.

Chargeable income band | Income in band | Exempt amount | Taxable after exemption |

|---|---|---|---|

First $10,000 | $10,000 | 75% x $10,000 = $7,500 | $2,500 |

Next $190,000 band | $110,000 | 50% x $110,000 = $55,000 | $55,000 |

Total | $120,000 | $62,500 | $57,500 |

The gross tax is then:

$57,500 x 17% = $9,775

This is already very different from the rough mental estimate of $120,000 x 17% = $20,400. The exemption scheme matters.

Partial Tax Exemption vs Start-Up Tax Exemption

Most companies can look at partial tax exemption. Some qualifying new start-up companies may use the tax exemption scheme for new start-up companies for their first 3 consecutive YAs.

For YA 2020 onwards, IRAS describes the start-up exemption as:

- 75% exemption on the first $100,000 of normal chargeable income; and

- 50% exemption on the next $100,000 of normal chargeable income.

Using the same $120,000 chargeable income, the comparison looks like this.

Scheme | Exempt amount on $120,000 | Taxable after exemption | Gross tax at 17% |

|---|---|---|---|

Partial tax exemption | $62,500 | $57,500 | $9,775 |

Start-up tax exemption, if eligible | $85,000 | $35,000 | $5,950 |

Do not assume a new company automatically qualifies for start-up exemption. Eligibility can depend on conditions such as the company’s shareholding structure and business type. When in doubt, verify against IRAS rules before relying on it.

Use the Corporate Income Tax Calculator

Once you understand the flow, use SBO’s Corporate Income Tax Calculator to test your own figures.

The calculator is useful when you already have an estimate of chargeable income and want to compare partial tax exemption, start-up tax exemption, tax set-offs and YA rebate settings. It is not a replacement for your tax computation, but it helps you see how the moving parts affect the final estimate.

A good workflow is:

- Prepare your accounts and tax adjustments.

- Estimate normal chargeable income.

- Choose the exemption scheme you believe applies.

- Review current YA rebate settings.

- Compare the calculator output against your accountant’s tax computation or IRAS filing.

What Legal Tax Reduction Actually Means

Reducing tax legally does not mean hiding income, creating fake invoices or mixing personal spending into the company. It means using the deductions, allowances and reliefs that the law already allows, with proper records.

Here are practical areas to review.

Area | Lawful action | What to watch |

|---|---|---|

Business expenses | Claim expenses that are wholly and exclusively incurred in producing business income. | Keep invoices, contracts, receipts and clear business purpose notes. |

Private or mixed expenses | Separate personal spending from company spending. | Meals, travel, phones and vehicles can become messy if business purpose is unclear. |

Fixed assets | Review capital allowance claims for qualifying fixed assets. | Accounting depreciation is not the same as a tax deduction. |

Approved donations | Consider qualifying donations to approved IPCs if they fit your company’s values and cash flow. | IRAS states qualifying donations can enjoy tax deductions of up to 2.5 times the donation amount. |

Unutilised losses and allowances | Review whether unutilised items can be carried forward, carried back or transferred through group relief. | Conditions such as shareholding tests and same-trade rules can apply. |

Government schemes and incentives | Check whether genuine activities qualify for grants, allowances or incentives. | Do not structure transactions purely to chase tax benefits without substance. |

Common Mistakes Singapore SMEs Make

The first mistake is applying 17% directly to revenue. Revenue is not profit, and profit is not automatically chargeable income.

The second mistake is assuming all expenses in the accounts are tax-deductible. Some expenses may need to be added back. Some asset purchases may need to be handled through capital allowances instead of normal expense deduction.

The third mistake is assuming start-up exemption always applies. It is a powerful scheme, but only if the company qualifies.

The fourth mistake is forgetting that rebates can change by Year of Assessment. A tax estimate built on last year’s rebate can be wrong for this year’s filing.

The fifth mistake is treating the calculator result as the final tax bill. A calculator can help you plan, but IRAS assesses the final position from your filed ECI or Form C-S/Form C-S (Lite)/Form C and supporting computation.

A Simple Tax Planning Checklist

- Close your accounts early enough to review tax adjustments calmly.

- Keep receipts and invoices in a searchable system, not in scattered chats and emails.

- Tag expenses by business purpose, especially for travel, meals, marketing and subscriptions.

- Review fixed asset purchases before year end so capital allowance treatment is clear.

- Check whether unutilised losses, capital allowances or donations exist from prior years.

- Confirm whether partial tax exemption or start-up tax exemption applies.

- Use the Corporate Income Tax Calculator for a planning estimate, then verify against IRAS or a tax adviser.

Final Thought

Corporate income tax becomes less frightening when you stop treating it as one mysterious percentage. Think in stages: accounting profit, tax adjustments, chargeable income, exemption scheme, 17% tax, rebates and set-offs.

That mental model helps you ask better questions, plan cash flow earlier, and avoid both overpaying from ignorance and underpaying from careless assumptions.

Singapore Corporate Income Tax FAQ

Is Singapore corporate income tax 17% of revenue?

No. The 17% corporate income tax rate applies to chargeable income, not revenue. You first need to account for deductible expenses, non-deductible add-backs, capital allowances, reliefs and exemption schemes.

What is partial tax exemption for Singapore companies?

For YA 2020 onwards, partial tax exemption generally exempts 75% of the first $10,000 of normal chargeable income and 50% of the next $190,000, before the remaining taxable amount is taxed at the corporate tax rate.

Do all new Singapore companies get start-up tax exemption?

No. Start-up tax exemption is only for qualifying companies and generally applies to the first 3 consecutive Years of Assessment. Always check the current IRAS conditions before assuming eligibility.

How can a company reduce tax legally in Singapore?

Common lawful methods include claiming allowable business expenses, reviewing capital allowances for qualifying fixed assets, using approved donation deductions, and applying unutilised losses or group relief only where the company meets the relevant conditions.

Can I rely on a corporate income tax calculator for filing?

Use a calculator for planning and sense-checking. Your final tax position should be based on your accounts, tax computation, IRAS rules and any advice from a qualified tax professional.

Sources Checked

- IRAS corporate income tax rate, rebates and tax exemption schemes

- IRAS basic guide to corporate income tax for companies

- IRAS business expenses

- IRAS claiming allowances

- IRAS donations and tax deductions

Explore More Content

Table of Content